UK Rental Market 2026: Legal Limits on Rent Increases for Landlords

Now that the Renters’ Rights Act has come into force, rent increases have just got far more regulated.

The Act introduced clearer rules designed to protect tenants from unfair or excessive rises.

Rent increases are now a more formal legal process governed by strict rules.

For landlords, this means rent reviews must be approached carefully and formally. But with the correct procedures and market evidence, you can adjust rents confidently while staying within the law.

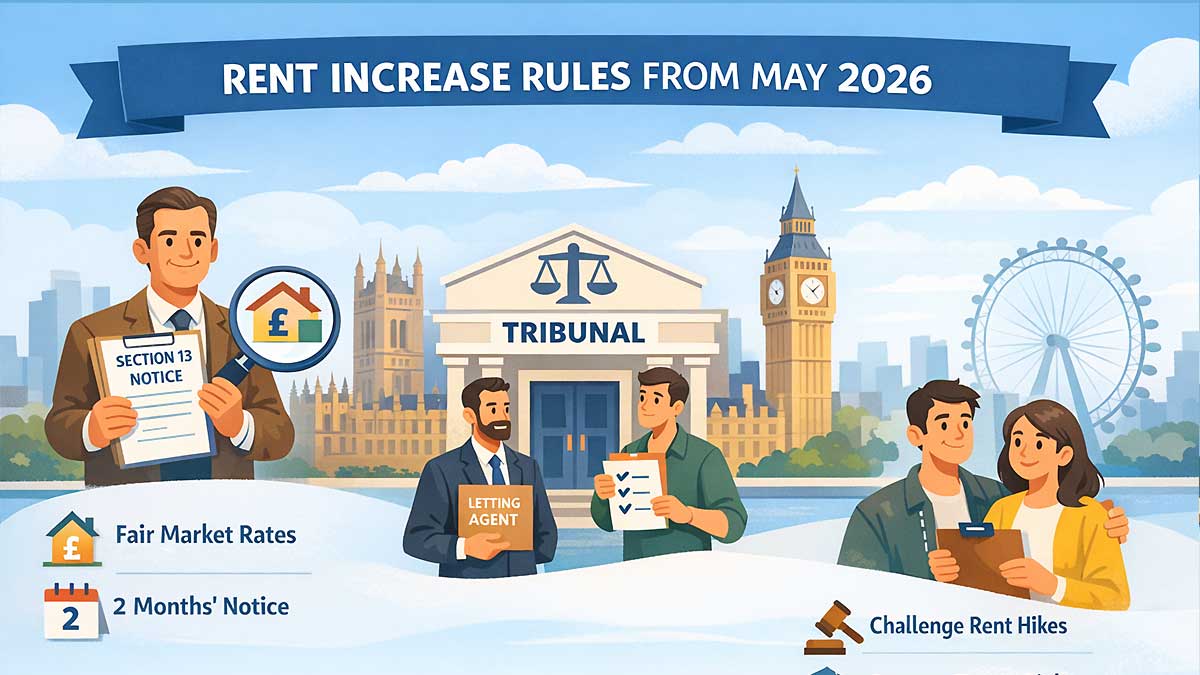

How often can I increase rent under the Renters’ Rights Act?

In most cases, rent can only be increased once per year. And there can be no increase within the first 52 weeks (1 year) of a new tenancy.

This removes the flexibility you might have previously relied on and reinforces the need to set realistic rents from the outset.

Contractual rent review clauses written into tenancy agreements will be abolished and rendered void under the new Act.

Attempting to increase rent more frequently, or without following the correct statutory process, could result in disputes or legal challenges.

Kristjan Byfield, Mission Commander at The Depository, issues a word of advice for landlords planning a rent increase:

“How your tenants are cared for during their tenancy will likely dictate how your rent review process will go. Make sure you have tenants that genuinely love living in your homes - and be fair when reviewing the rent.

“Tenants are about to decide when they leave and what a rent review process looks like, so give them every reason to stay.”

Let’s get into the rules about increasing rent under the Renters’ Rights Act.

When do I need to use a Section 13 notice?

Informal agreements, such as verbal conversations or casual emails, are no longer sufficient.

As all tenancies have converted to periodic (rolling) tenancies, you must always use the prescribed legal mechanism: a Section 13 notice.

This is a formal statutory document that clearly sets out the proposed new rent and the exact date it will take effect.

Finally, you should keep detailed records of all rent reviews, communications and any Section 13 notices you have served. This not only supports compliance but also provides protection in the event of a dispute.

How much can I increase rent under the Renters’ Rights Act?

You can increase rent up to the current fair market rate. That means you should go by what the property would fetch if it were newly advertised to let today.

Before proposing an increase, research local market rents and be prepared to justify your decision.

Letting agents can provide useful benchmarks, helping ensure your figures are realistic and defensible.

Under the new system, tenants have stronger rights to dispute rent increases they believe exceed market value.

These challenges may be referred to a First-tier Tribunal, which will assess whether the proposed rent aligns with comparable properties in the area.

Crucially, the Tribunal can no longer set the rent higher than what the landlord initially proposed, meaning tenants effectively have ‘nothing to lose’ by challenging a hike.

The Tribunal will also no longer backdate increases, and the new rent will only apply from the date of the Tribunal's decision.

When you’re thinking about increasing rent, it’s worth considering tenant relationships. While the law may allow for an increase, large or sudden jumps can lead to dissatisfaction, increased turnover and void periods.

That means a measured, market-aligned approach will be more sustainable in the long term.

How much notice must I give before increasing rent?

Under the Renters' Rights Act 2025, the mandatory notice period for a Section 13 rent increase has been extended. You must provide your tenant with 2 months' written notice before the new rental amount comes into effect.

This notice period gives tenants more time to review the increase and, if necessary, challenge it.

How can a letting agent help with increasing rent?

Navigating the new legal landscape of the Renters' Rights Act can feel daunting. Rent reviews are now a strictly regulated legal procedure, so leaning on a professional letting agent can help protect your investment.

A good agent takes the guesswork out of the process by providing accurate, evidence-based market valuations. Since the new rules cap rent hikes at the current market rate, an agent’s access to hyper-local data ensures your proposed increase is fair, defensible and less likely to be challenged at a tribunal.

If a tenant does dispute the increase, your agent will be invaluable in compiling the necessary portfolio of comparable properties to justify the new rent. This handles any pushback objectively, preserving your relationship with the tenant and turning a potential legal minefield into a smooth, fully documented process.

Kristjan’s top tip for those already using a letting agent? Take this chance to get your tenants’ perspective.

“If you have a managing agent, now might be a good time to reach out to your tenants directly to see what their rental experience is like. There’s nothing like hearing things first hand and the Act means that great rental experiences will be even more vital in shaping top-performing property portfolios.”

Prefer to self-manage? Success comes down to meticulous preparation. You will need to track local market rents and ensure your figures are justifiable.

It’s also highly recommended that you join a professional body, such as the National Residential Landlords Association (NRLA), to ensure you have access to the correct Section 13 templates and a reliable support network should you need to defend an increase at a First-tier Tribunal.

Key takeaways

- From 1 May 2026, rent cannot be increased within the first year of a tenancy, and only once a year after that, using a Section 13 notice

- Proposed increases cannot exceed the current fair market rate

- Tenants now have stronger, risk-free rights to challenge hikes at a tribunal

- You must give tenants a full 2 months' written notice before an increase takes effect

- Documentation, market research and professional support can help you adjust rents while staying within the law

Renters’ Rights Act 2026 Explained, Key Changes Every Tenant and Landlord Should Understand

The Renters’ Rights Act came into force on 1 May 2026, bringing significant changes for tenants, landlords, and the wider lettings market across the UK. This guide outlines the key reforms, including the abolition of ‘no-fault’ evictions, new limits on rent increases, and updated rules around requests such as keeping pets.

Do you know how the Renters’ Rights Act will affect your tenancy? Or are you a landlord looking to get to grips with the new regulations?

Our guide to what’s changing will help you navigate your renting journey, whether you're new to renting, an existing tenant or renting out your property as a landlord.

What is the Renters’ Rights Act?

The Renters' Rights Act 2025 is a landmark piece of UK housing legislation designed to reform the private rented sector.

Having received Royal Assent in October 2025, the Act represents the most significant update to tenant and landlord laws in nearly 40 years.

The Act introduces a lot of changes that affect both landlords and tenants. Its primary purpose is to rebalance the rental market, providing more security and stability for private renters across England.

When does the Renters’ Rights Act start?

The Renters’ Rights Act will come into effect in phases. The first big milestone is 1 May 2026, bringing in new rules including those for evicting a tenant and the switch from fixed terms to periodic tenancies.

There will be more changes later in 2026, including a new ombudsman. And beyond that, there will be new EPC rating requirements and a Decent Homes Standard.

Renters’ Rights Act changes from 1 May 2026

New eviction process

Landlords now need a valid reason to evict a tenant, known as a ground for possession. You can find a list of the new, revised and existing grounds on the government’s website. There are new notice periods too, which may allow you to stay in your home for longer.

Landlords are still allowed to sell their property but they won’t be able to use this reason during the first 12 months of a tenancy. In addition to waiting 12 months, your landlord must give you at least 4 months’ notice.

Notice periods do depend on the reason for the eviction. If you are involved in severe anti-social or criminal behaviour, for example, your landlord doesn’t need to give any notice.

Evictions for rent arrears

A landlord can use Ground 8 (severe rent arrears) to evict you but they now have to wait longer to serve notice. This gives you more time to repay arrears.

A landlord can only use Ground 8 once you owe at least 3 months’ rent (or 13 weeks’ rent for a weekly tenancy). The notice period for severe arrears is also doubling, from 2 weeks to 4 weeks.

Landlords can use Ground 10 if you have arrears of less than 3 months, or Ground 11 if you frequently pay your rent late. It would, however, be up to a court to decide if the landlord’s eviction request was reasonable.

Challenging evictions

You can still challenge a landlord’s decision to evict you in court. This applies if you think your landlord is acting unfairly or if they haven’t followed the correct eviction procedure.

End of fixed-term tenancies

‘Rolling’ periodic tenancies have now become the only type of contract offered. If you currently have a fixed term tenancy, it automatically switched to a periodic one on 1 May 2026.

Periodic tenancies allow you to end your tenancy when it suits you, as long as you give your landlord 2 months’ notice.

Bidding wars banned

The price you see a property advertised for is the price you will pay, thanks to the new ban on bidding wars between tenants.

Landlords and letting agents have to set an asking price and stick to it. They must refuse higher offers, even if the tenant is willing to pay more.

Rent increase limits

Landlords are now limited to increasing your rent to once a year, using a Section 13 notice. And when they do so, they must set an increase that’s in line with local market rates.

If you think a rent increase is unreasonable, you can challenge it at the First-tier Tribunal. A challenge will be at a low fee, with no hearing cost.

Cap on rent in advance

Rent in advance is now capped at 1 month’s rent. The limit is designed to prevent tenants overcommitting themselves financially.

Rent in advance is usually paid between signing the agreement and the tenancy starting. You can still volunteer any sum of upfront rent during your tenancy.

End to discrimination

You cannot be excluded from the rental market just because you have children or receive benefits. Rental discrimination is now banned, with decisions based on affordability and referencing.

Right to request a pet

You now have a new right to request to keep a pet after you’ve moved into a property. Your landlord must consider the request. If they refuse, they have to give you a valid reason in writing.

You can also take action if you think your landlord’s pet refusal is unfair. Complaints can be lodged with a new private rented sector ombudsman or taken to court.

Renters’ Rights Act changes later in 2026

Private rented sector ombudsman

Later in 2026, you’ll have free access to a new private rented sector ombudsman. Landlords will be obliged to sign up.

The ombudsman will handle complaints about fees, maintenance, compliance and communication. The aim will be to avoid disputes going to court.

Private rented sector database

A new private rented sector database will launch later this year. Like the ombudsman, landlords will have to sign up.

The database will be free and open for tenants to use. You’ll be able to check who you’re renting from and see documents about property standards.

Renters’ Right Act changes in the future

A new EPC grade

Lower fuel bills and reduced carbon emissions will become a reality for more renters. By 2030, most privately rented homes will need an EPC rating of C or better. Your landlord will be responsible for making eco improvements.

Decent Homes Standard

Every privately rented home will eventually need to meet a new Decent Homes Standard. Landlords will become legally obliged to ensure their properties are safe, secure and hazard free.

Awaab’s Law

Awaab’s Law will empower tenants to challenge dangerous conditions. It will also force landlords to make repairs within a set time period.

Key takeaways

- Most reforms came into effect on 1 May 2026, giving tenants new rights and better protection

- Rent increases are now limited to once a year and rent in advance is capped to 1 months’ rent

- ‘No fault’ evictions are now banned. Instead, landlords must have a valid reason from a Government list to evict a tenant

- Landlords can no longer discriminate against tenants with children and those receiving benefits

- Future reforms include a new landlord database and an ombudsman, so renting becomes a safer and more transparent experience

- If your tenancy started before 1 May 2026, your landlord or letting agent must send you an information sheet by the end of May 2026 to confirm what’s changing with your contract

Deposit Protection Schemes Explained

Moving into a rented property in the UK? Here’s what tenants need to know about tenancy deposits, your legal rights, and how landlords are required to protect your money through a Government-approved deposit protection scheme.

If you rent your home, your landlord usually has to keep your deposit safe by using one of the government's deposit protection schemes.

Here's everything you need to know about deposits when you rent a home and the protection schemes that keep your money safe.

What is a deposit?

A deposit is typically the equivalent of up to 1 month's rent and has been capped at 5 weeks' rent since 2019.

You give your landlord a deposit to protect them against any breaches of your tenancy agreement. This includes damage to the property, additional cleaning or covering unpaid bills once you've moved out.

While you're in the rental home, the deposit remains your property. And it should always be returned at the end of the tenancy, provided you have stuck to the rental agreement.

It is not law to have an inventory to use a deposit protection scheme, but it is good practice.

An inventory documents the condition of the property and its contents at the start of a tenancy. It's very helpful if there's a dispute at any point.

The inventory should be signed by both landlord and tenant. If you do not use an inventory, take photographs of the property inside and out at the start of a tenancy to keep a record.

You should also check your rental contract for the circumstances in which the landlord can make a claim on your deposit.

How to understand your rental contract

How does a deposit protection scheme work?

In the past, a landlord was able to withhold an entire deposit at the end of a tenancy if they were in dispute with the tenant.

In rare cases, this could lead to unscrupulous landlords taking advantage of honest tenants.

So the government introduced tenancy deposit protection in 2007 in a bid to regulate the system.

As a result, a landlord must protect their tenant’s deposit using an approved deposit protection scheme.This applies to the large majority of private renters.

Historically, this rule applied to tenants on an Assured Shorthold Tenancy (AST) created after 6 April 2007. However, since the Renters' Rights Act in May 2026 abolished ASTs in favour of standard rolling contracts, the deposit protection rules now apply universally to all private periodic assured tenancies.

These conditions do not apply in some cases, such as when a landlord lives in the property with the tenant, or if the tenant lives in student halls of residence. However, it is still regarded good practice to ensure deposits are protected.

What are the 3 deposit protection schemes?

There are 3 government-backed deposit protection schemes operating in England and Wales:

The schemes aim to help safeguard deposits and provide an even and effective means of resolving disputes between the landlord and tenant.

They also hope to promote greater understanding between both parties at the start of a tenancy.

Make sure your landlord is using one of these 3 schemes if you live in England or Wales. If any other scheme is used, then your deposit is not protected by law.

There are separate tenancy deposit protection schemes in Scotland and Northern Ireland.

What types of deposit protection schemes are there?

All 3 of the government-backed tenancy deposit protection schemes offer custodial and insurance-based options.

1. Custodial

The custodial option is where the landlord lodges the deposit with the scheme for the duration of the tenancy.

The money is then released when both the landlord and tenant agree on the total sum to be returned at the end of the tenancy.

The custodial option is free for landlords to use because it is funded by interest made on the deposit.

Landlords based overseas must use the custodial format unless they employ a British-registered letting agent to manage their tenancy.

2. Insurance

The insurance option is where the landlord holds the tenant's deposit throughout the tenancy and pays the scheme a fee to have it protected.

The landlord manages the repayment at the end of the tenancy.

If the landlord does not pay the tenant the amount they are owed, then the scheme will pay the tenant and try to get the money back from the landlord.

What happens at the start of a tenancy?

As a tenant, you might pay a holding deposit before you sign a rental agreement. This reserves the property for you, but landlords are not required to protect it until you become a tenant.

Your holding deposit can be no more than 1 week's rent.

Once you sign a rental agreement, you pay the main deposit, which is usually called either your tenancy or security deposit. This must be protected with a scheme.

The landlord might put your holding deposit towards the tenancy deposit.

Landlords (or their letting agent) must put the deposit in one of the protection schemes within 30 days of receiving it.

The landlord can choose which deposit protection scheme they use and they have to inform you which one it is.

Landlords are still required to use a protection scheme even if your deposit is paid by a third party, such as your parents or guarantor.

Within 30 days of receiving a deposit, landlords must provide you with:

-

address of the rented property

-

deposit amount paid

-

how the deposit is protected

-

name and contact details of the deposit protection scheme and its dispute resolution service

-

landlord or letting agent’s name and contact details

-

name and contact details of any third party that has paid the deposit

-

why they would keep some or all of the deposit

-

how to apply to get the deposit back

-

what to do if a tenant cannot get hold of the landlord at the end of the tenancy

-

what to do if there is a dispute over the deposit

If you do not receive this information within 30 days, follow up with your letting agent or landlord.

How long is the deposit protection scheme valid for?

Your deposit is protected for the duration of your tenancy with the same landlord. It will remain protected on a continuous, rolling basis until you eventually move out.

What happens if a landlord is suspected of not using a deposit protection scheme?

If you believe your landlord has not used a deposit protection scheme when they should have done, you can apply to the local county court at any time during the tenancy.

Inform the landlord first to give them the opportunity to protect your deposit with a scheme.

You should get legal advice if you feel you need to apply to court.

The court has the power to order the landlord to repay the deposit to you or put it into a custodial tenancy deposit protection scheme bank account within 14 days.

The court can also order a landlord to repay you up to three times the original deposit as a fine within a fortnight.

What happens at the end of a tenancy?

As a tenant, you should be told how much of your deposit is going to be returned to you within 10 days of the end of the tenancy.

The deposit is normally paid into your bank account.

The government-backed schemes mean that you will get your deposit back based on the following conditions:

-

the terms of the tenancy agreement are met

-

there is no damage done to the property or contents

-

the rent and bills are paid

Solving a dispute

Each deposit protection scheme offers a dispute resolution service, known as Alternative Dispute Resolution.

The service can be used if you and the landlord are in disagreement about how much deposit should be returned at the end of a tenancy. It is a free service and is intended to resolve disagreements without the need to go to court.

There may be a time limit on when a dispute must be registered by. Landlords and tenants are advised to contact the tenancy deposit protection scheme as soon as possible.

Cleaning charges and general wear and tear are among the more common reasons for deposit disputes. The government defines the phrase as "reasonable use of the premises by the tenant and the ordinary operation of natural forces".

It is a legal principle too that you should not bear the full cost of having any part of a property, or any fixture or fitting, put back to the condition it was at the start of the tenancy agreement.

The dispute resolution service differs slightly, depending on which scheme the deposit is held in. However, the overarching principles remain the same.

The service can only be used if both you and your landlord agree to use it and accept the ultimate decision made.

If a dispute arises, you and the landlord are both required to provide evidence to an impartial and qualified adjudicator within the required timescale.

Adjudicators can be individuals hired under contract to the deposit protection scheme or employed directly by the scheme.

Both you and the landlord should try to see the evidence from the independent third party or adjudicator's perspective. How will they view a case?

Types of evidence can include:

-

tenancy agreement

-

inventory

-

photo or video evidence

-

invoices, receipts and quotes

-

bank statements

-

utility bills and council tax

-

witness statements

You and the landlord are not required to meet during the process, and the adjudicator will not visit the property in question. The adjudicator will decide the final outcome.

The adjudicator will consider a number of factors, likely to include:

-

length of tenancy

-

number and age of tenants

-

quality and condition of property and/or fixtures and fittings

-

wear and tear of property and/or fixtures and fittings or damage

The onus is on the landlord to show that he or she has a justifiable claim to retain all or part of the deposit, as the money remains your property.

If you or the landlord don't agree to use the deposit scheme's dispute resolution service, you may need to escalate the issue. Rather than jumping straight into stressful and expensive court action, you can now take your complaint to the Private Rented Sector Landlord Ombudsman (introduced under the Renters' Rights Act 2026), which is completely free for tenants to use and has the power to compel landlords to resolve financial disputes.

Landlords are responsible for making sure the deposit is kept safe with one of the schemes even if they use a letting agent to look after the deposit, which provides you with peace of mind.

It's worth taking the time to explore the different schemes available and see which is best, considering the property, the rental agreement and the landlord's own situation, to make the right choice.

You can get further help and advice from:

-

a solicitor

-

Shelter in England or Wales

Key takeaways

- You pay a tenancy deposit to protect the landlord against breaches of your agreement, like damage, additional cleaning or covering unpaid bills

- The landlord must use one of 3 government-backed protection schemes and provide you with the details

- You should be told how much of your deposit is going to be returned to you within 10 days of the end of the tenancy

- If there's a dispute when you move out, you can use a resolution service provided by the deposit protection schemes

Tenancy Paperwork Explained

Secured Your New Rental Property? Explore Everything You Need to Know About Referencing, Tenancy Agreements, Moving In, Maintenance Reporting, and Moving Out

From references and deposits to inventories and tenancy agreements, renting a property involves a bit of paperwork at the beginning and end of your rental agreement.

And in between all that, there are yours and your landlord's rights and responsibilities to consider.

Here's our guide on how renting a property works and all the paperwork you need to be aware of.

Securing a property to rent

Begin by putting down a holding deposit in order to state your intention to rent the property and have it taken off the market. This is capped at one week’s rent and is refundable after 14 days.

Don't forget to check whether there are any other letting agents marketing the same rental home.

The letting agent or landlord will then begin the administrative process of requesting references from you.

References

Your prospective new landlord will be keen to make sure that you are a suitable tenant and that you have the ability to pay your rent. They may also be interested in whether you have rented a property without any major problems in the past.

The landlord or, if instructed, the letting agent will organise the reference checks and may ask for your permission to conduct the relevant searches.

In the past, they may have asked for an administrative fee from you to conduct these checks but they are no longer allowed to do so.

In fact, all agency fees have now been banned, and under the Renters' Rights Act implemented in May 2026, bidding wars were also outlawed. This means the only upfront cost you should be asked for at this stage is the holding deposit based on the advertised rent.

Some or all of the following documents may be requested by the letting agent or landlord:

-

References from previous landlords - you may be asked to give the details of where you have lived within the last three years

-

A credit check - this will allow them to see if you have a good history of paying your bills.

-

Your bank details, including the bank name, account number and sort code

-

Details of your employment, including your employer, job title, payroll number, salary and previous employer

-

Proof of your right to rent in the UK (often requiring a digital 'share code' from the Home Office)

Under the Data Protection Act, you can only be asked for information that is required for the tenancy, and it must be stored securely and checked regularly to make sure it is still needed and is accurate.

Landlords are also legally banned from having blanket policies that discriminate against families with children or people on benefits.

In the event that the information highlights any potential of risk to the landlord, you may be asked to provide a guarantor.

A guarantor will be contractually liable, both financially and legally, should you fail to pay the rent during your tenancy or in the event of damage to the property.

The deposit and upfront payments

The final part in securing the property is putting down the deposit, which you will be asked for once you have signed a contract.

This deposit is capped at 5 weeks’ rent, unless your rent is more than £50,000 a year, in which case you may be asked for 6 weeks’ rent.

A landlord is also legally restricted from asking for more than 1 month's rent in advance.

The deposit is a safety net for the landlord to guard against the cost of replacing or repairing property damaged by you.

-

Landlords and letting agents in England are required to join one of the Government-backed tenancy deposit protection schemes

-

You must be given proof that your deposit has been put into one of these schemes within 30 days of you paying it

-

You will get all or part of your deposit back at the end of the tenancy if you have kept the rental property in good condition

-

The schemes offer alternative ways of resolving disputes which aim to be faster and cheaper than taking court action

The deposit and upfront payments

The final part in securing the property is putting down the deposit, which you will be asked for once you have signed a contract.

This deposit is capped at 5 weeks’ rent, unless your rent is more than £50,000 a year, in which case you may be asked for 6 weeks’ rent.

A landlord is also legally restricted from asking for more than 1 month's rent in advance.

The deposit is a safety net for the landlord to guard against the cost of replacing or repairing property damaged by you.

-

Landlords and letting agents in England are required to join one of the Government-backed tenancy deposit protection schemes

-

You must be given proof that your deposit has been put into one of these schemes within 30 days of you paying it

-

You will get all or part of your deposit back at the end of the tenancy if you have kept the rental property in good condition

-

The schemes offer alternative ways of resolving disputes which aim to be faster and cheaper than taking court action

The inventory

This is one of the most important documents in the renting process and can be key in deciding how much of your deposit is returned at the end of your tenancy.

You should be extremely thorough and give it your full attention, while taking the necessary precautions to protect your interests.

How is the inventory prepared?

The inventory is a simple list detailing every item contained within the property and the condition each listed item is in, as well as the state of the property itself, on the day you move in.

This may be prepared by either the letting agent or the landlord. Either way, you should go round the property with the landlord or agent and agree the state of each item before signing anything.

If necessary, take photographic or video evidence to give you extra protection and avoid any unnecessary disagreement at a later stage.

You will be expected to sign the inventory and initial every page, along with the landlord or letting agent.

When will the inventory be checked again?

It is not uncommon for landlords and letting agents to schedule in regular three-monthly inventory checks at the property in order to assess any damage that may have occurred.

Find out if there are regular checks planned and when they will take place. It is most common, however, for a final inventory check to take place on the day you are scheduled to move out.

Tenancy agreements

The tenancy agreement is a legally-binding contract between you and the landlord.

It specifies certain rights to both you and the landlord, such as your right to live in the home for the agreed term and your landlord's right to receive rent for letting the property.

Significant changes to tenancy agreements came in from 1 May 2026 with the Renters' Rights Act. Assured Shorthold Tenancies (ASTs) were abolished and the standard contract is now the Assured Periodic Tenancy.

The most important aspect of this agreement is that there is no fixed end date and no minimum term. The tenancy rolls on a monthly basis. Landlords lost the right to automatically repossess the property at the end of a term without a reason when 'no-fault' Section 21 evictions were banned.

The 2026 laws also made consent for pets a legal right. In practice, this means landlords cannot issue a blanket ban on tenants with pets and cannot unreasonably refuse a written request to keep one, though they can ask you to carry pet insurance.

There are specific requirements linked to the tenancy that include:

-

The tenant(s) must be an individual(s) (not a business or entity)

-

The property must be the main home of the occupant(s)

-

The property must be let as separate accommodation

-

The tenant must provide the landlord with 2 months' notice if they want to terminate the agreement at any time

-

The landlord must provide a valid legal reason (such as selling the home or moving back in) to terminate the agreement, which typically requires them to give 4 months' notice.

The agreement will most likely contain the following information:

-

Your name, your landlord's name and the address of the property which is being let

-

The date the rolling tenancy will commence

-

The amount of rent payable, how often it should be paid, when it should be paid and when it can be legally increased (which is now limited to once a year via a Section 13 notice)

-

What payments are expected, including Council Tax, utilities and service charges

-

What services your landlord will provide, such as maintenance of common areas

Tenant and landlord rights and responsibilities

The responsibilities of both parties are likely to be detailed within your tenancy agreement, although some conditions may vary between properties and landlords.

Preparing to move in

When all the paperwork has been completed, it's time to move in. Check out our top tips for making the moving in process as easy as possible.

Moving out

When you're thinking about moving out, it's important to remember you have the right to stay as long as you like.

As tenancies are now all rolling agreements, there is no end date that you need to renew or extend. Providing you adhere to your tenancy agreement, you can simply continue your occupancy. Your landlord cannot ask you to leave simply because a certain amount of time has passed.

Or, you can give 2 months' notice in writing if you decide to move out.

Leaving the property in the right condition

It's worth putting in a bit of work to get the property up to scratch to maximise the chances of getting your full deposit back.

As long as the condition of the property is the same as when you moved in (barring normal wear and tear), you should have no problem. So here's what you should do:

-

Give the property a thorough clean, including carpets, windows, walls and furniture

-

Clear away any rubbish

-

If it's your responsibility, tidy up the garden

-

Remove all your personal belongings

-

Be satisfied you're leaving the property as you found it

Return all the keys to the landlord

If you decide to move out, it's worth putting in a bit of work to get the property up to scratch to maximise the chances of getting your full deposit back.

As long as the condition of the property is the same as when you moved in (barring normal wear and tear), you should have no problem. So here's what you should do:

-

Give the property a thorough clean, including carpets, windows, walls and furniture

-

Clear away any rubbish

-

If it's your responsibility, tidy up the garden

-

Remove all your personal belongings

-

Be satisfied you're leaving the property as you found it

-

Return all the keys to the landlord

Final inventory check

You'll have the opportunity to run through the inventory checklist on the day of departure.

It's important that this job is done as you leave the property, to avoid you being accountable for any damage that occurs after you've left.

If there is any damage, you should agree with the landlord the cost of repairing or replacing such items.

If an agreement cannot be reached as to the damage of particular items, which items have been damaged, or repair costs, then you should make sure you take photographs.

Get your own repair cost estimates and write to the landlord with your findings and work towards a mutually agreeable solution. If you still cannot reach an agreement, you can refer the dispute to the tenancy deposit protection scheme.

If both you and the landlord are satisfied the property has been left in an acceptable state and you have made your final rental payment, there should be no problem getting your deposit back.

Arranging viewings safely

When arranging viewings, it’s sensible to follow a few safety principles.

It’s always a good idea to take someone with you to a viewing. After all, it’s handy to have a second opinion, right?

Let a friend or relative know where you are, what you’re doing and that you’ll give them a quick call when you’re done. You can use certain apps, such as WhatsApp, to share your location for extra peace of mind.

If you're looking at a room share, ask to meet everyone who lives or will be living at the property. This will help you get to know all of your potential flatmates and gives you a sense of their characters.

Remember if you feel at all uncomfortable, you can leave the viewing at any time. Always trust your instincts – if something doesn’t feel right, it’s time to go.

Key takeaways

- You will now always sign an Assured Periodic Tenancy agreement, meaning your paperwork will reflect a rolling monthly contract with no fixed end date

- Have your bank details, employer references, and digital 'share code' (for Right to Rent checks) ready to go, and remember that agents cannot legally charge you admin fees to process them

- Ensure your tenancy agreement does not ask for more than 1 month's rent in advance or a deposit larger than 5 weeks' rent, as both are now strict legal limits

- Treat this document with extreme care, take supporting photos, and ensure every page is initialled before moving in to protect your deposit when you eventually leave

London in Bloom: Signature Experiences for May 2026

As the capital transitions into the summer season, May 2026 presents a prime window to capitalise on open-air festivals, elevated rooftop venues, and high-profile cultural exhibitions.

May stands as a cornerstone in London’s annual calendar—where operational tempo increases, consumer sentiment lifts, and the city’s full commercial and cultural potential begins to surface. With favourable weather conditions and the capital in full spring bloom, there is a tangible sense of momentum as Londoners and visitors alike anticipate the summer season.

Crucially, the dual bank holidays create extended windows for leisure engagement and footfall across hospitality and entertainment sectors. This period consistently drives strong performance for rooftop venues, early-season music festivals, public green spaces, and flagship exhibitions. It also presents a strategic opportunity for short-haul travel, with many opting for curated day trips or premium mini-breaks.

To ensure optimal utilisation of the month, we’ve consolidated a forward-looking guide to London’s key events, activations, and experiential offerings for May 2026. From high-energy festivals to limited-time pop-ups and cultural highlights, the city is positioned to deliver a high-impact, high-enjoyment cycle.

1. Dance to sets from George Daniel, Call Super and Chaos in the CBD at GALA

All of London’s hottest and hippest people will head to Peckham Rye Park for one of London’s best electronic music bonanzas in May. GALA will return after its hugely successful 10th anniversary event in 2025. The theme for 2026 has been revealed as The Floor Is Ours, which is a call for community and creative ownership, and wants to take a stand against the growing commercial tide in dance culture.

Friday’s bassier line-up features Benji B, Or:La and Charlie xcx’s hubby George Daniel. Peach will debut her new Dreamland project on the Saturday with a takeover of the Pleasuredome. She’ll be joined on the line-up by Call Super, Prosumer, Job Jobse and Steffi x Virginia. And Sunday will go hard on the disco and house, with a rare b2b2b from Hunee, Palms Trax and Antal, plus Chaos in the CBD and Moxie, who will bring her On Loop party to the festival.

2. See the musical version of a Tim Burton classic

There are only so many theatres in London big enough to stage a proper full on Broadway musical spectacular, and with MJ the Musical off, the door is open for Beetlejuice the Musical to enter.

The name ought to make it pretty clear what we’re talking about here: Beetlejuice is of course Tim Burton’s cult classic 1988 film about a young couple with a very nice house who die in a car crash and are horrifed to observe – from a very surreal, bureacracy-bound afterlife – that some ghastly new people have moved into their old gaff.

The stage version is directed by Alex Timbers, best known to London audiences for his heroically OTT smash Moulin Rogue! The Musical – you can expect similar amounts of excess here.

3. Attend the Glastonbury of gardening, the RHS Chelsea Flower Show

Every spring, west London hosts the Glastonbury of thegardening calendar. Across five days, hundreds of world-class growers and garden designers descend on Chelsea’s Royal Hospital Grounds to take part in the floral extravaganza that is the RHS Chelsea Flower Show.

More than 400 exhibits will show off the green-fingered talent of the world’s finest landscapers and horticulturalists, and shine a spotlight on charities such as Parkinson’s UK, the Trussell Trust and Asthma + Lung UK. Then, of course, there’s the much anticipated (and rather frantic) plant sell-off on the final day of the event when exhibitors put their display plants up for bargain prices.

4. Bag a ticket to surprisingly enjoyable sequel The Devil Wears Prada 2

Isn’t it lovely when things turn out better than you imagined? Meryl Streep and Anne Hathaway are reunited for this updated on the classic fashion world caper, which has all the sass and energy of the 2006 original but none of the lazy repetition and box-ticking fan service that blights this kind of reboot (Tron, Ghostbusters, any number of Halloween movies). Dig your cerulean sweater for a cinema trip with undeniable style.

5. Catch Floating Points, Honey Dijon and Joy Orbison at Field Day

Field Day tried to get back to its roots in 2025 when it up sticks from its more corporate-feeling Victoria Park set up and went to Brockwell Park. It will return to south London in May, so get it locked in the diary. On the line-up for 2026 is a dependable selection of DJs and producers, with the biggest names including Andy C, Floating Points, Honey Dijon and Joy Orbison. They’ll be joined by Anish Kumar, Interplanetary Criminal, KI/KI, sim0ne, Eliza Rose, Horse Meat Disco and others for a day of non-stop dancing.

6. Catch buzzy young playwright Ava Pickett’s West End debut

Much-hyped young playwright Ava Pickett’s superb debut play 1536 follows three young women who meet at the outskirts of an Essex village to discuss love, life and Anne Boleyn’s execution. It’s a brilliant, bold debut play featuring some bleakly astute observations on the power dynamics between men and women that go considerably beyond the Early Modern Period, it was a hit for the Almeida, it transfers to the West End’s Ambassadors Theatre this month.

7. Don’t miss the final days of a major Catherine Opie retrospective

The National Portrait Gallery is as much a monument to national identity as it is an art gallery. It’s an education in our collective understanding of British life, culture and history. But who isn’t here? Who doesn’t get to shape the version of the nation’s identity on display to the thousands of tourists, school groups and art lovers who parade through these grand rooms every day? That question is central to the work of American photographer Catherine Opie, whose exhibition, To Be Seen, is currently installed on the second floor of the gallery. Not only does Opie's work serve to challenge visitors’ ideas about who belongs on the walls of this historic institution, but it also brilliantly elucidates the artist’s Baroque and Renaissance references.

8. Learn about Jurassic sea creatures at a new Natural History Museum exhibition

The Natural History Museum’s temporary 2026 exhibition offers a sop to the dinosaur-loving masses without technically being about dinosaurs, focussing instead on the weird, wonderful and terrifying world of prehistoric sea monsters. Think pliosaurs, think ichthyosaurs, think think mosasaurs – whose profile shot right up after being featured as the ultimate reptillian killer in Jurassic World. We’re not quite clear what this show will involve specifically at this stage, but the NHM’s temporary exhibitions are always a delight, far more spacious and with far more technologically advanced interactive exhibits than its delightful but creaky dinosaur room.

A Landlord’s Guide to Avoiding Missteps in the Renters’ Rights Act

From 1 May 2026, the Renters’ Rights Act introduces significant reforms to England’s private rental sector, with tighter regulations and increased legal accountability for landlords. Understanding the most common pitfalls will be essential to safeguard your investment and ensure full compliance.

The Renters’ Rights Act marks one of the most significant shifts in the private rented sector in England in decades.

The reforms go live from 1 May 2026 and aim to strengthen tenant protections, but they create new legal risks for landlords who fail to adapt to the new environment.

We've uncovered the key areas of risks for landlords to help you prepare for the changes and stay compliant under the Renters' Rights Act.

(That there are different regulations for landlords and agents operating in Scotland and Wales. This article only talks about the upcoming changes in England.)

1. Misunderstanding how to regain possession of a rental property

The mistake: Assuming possession can still be regained quickly or informally, as under previous Section 21 processes.

The abolition of Section 21 means landlords must now rely on more structured Section 8 grounds. These include selling the property, moving in or tenant fault-based grounds such as rent arrears.

How to evict a tenant after 1 May 2026:

-

Ensure you are using the correct possession ground and that it applies legitimately.

-

Serve accurate and compliant notice periods (which may be longer than before).

-

Keep detailed documentation and evidence to support your claim (e.g. sale intent, arrears records).

-

Follow court processes carefully - errors can result in delays or case dismissal.

Possession is still possible - but only with proper justification, paperwork and patience.

2. Increasing rent incorrectly

The mistake: Raising rent informally, too frequently or without using the proper notice.

Rent increases will be limited to once per year, with stricter rules around fairness and transparency. Tenants may challenge increases they believe are above market levels.

How to avoid this mistake:

-

Use the correct legal mechanism, such as a formal notice procedure. When you are issuing a section 13 notice, make sure you use the new form 4A (not the current form 4).

-

Check how much notice you need to give and provide notice in writing. Notice periods are increasing from 1 month to 2 months and must be in line with the rent due date.

-

Ensure increases reflect local market conditions, not arbitrary figures. Remember market rent can go up as well as down, so knowing your local area will be vital.

-

Be prepared for potential tribunal challenges. Approach every rent increase with the assumption it will be appealed, so start compiling your defence bundle from the day you issue the section 13 notice.

Essentially, the changes mean it’s best to view rent reviews as a formal legal process, not a casual adjustment. Keeping rent low as a ‘favour’ to the tenants may not be an option going forward as this could risk the tenant getting stuck in a rent budget bubble, and not being able to move on if needed.

3. Failing to meet repair obligations on time

The mistake: Delaying repairs or underestimating how quickly issues must be resolved.

The Renters’ Rights Act strengthens expectations around property standards and response times, with greater enforcement powers for local authorities.

The repairs you’re responsible for as a landlord:

-

Structural integrity (roof, walls, windows)

-

Heating, hot water, plumbing and electrics

-

Safety hazards (e.g. damp, mould, fire risks)

The law does not say how long a reasonable time is. It depends how serious or urgent the problem is and how vulnerable the people living in the property are, but a good guideline is:

-

Emergency issues: within 24 hours

-

Urgent repairs: within a few days

-

Routine repairs: within a reasonable timeframe (typically 1–2 weeks)

How to avoid this mistake:

-

Implement a clear repair reporting system

-

Keep written records of all communications and actions, including any refusal for access or rescheduling

-

Work with reliable contractors for fast response

-

Conduct regular inspections

Speed and documentation are critical from 1 May 2026, and delays can lead to legal and financial consequences.

4. Overlooking compliance and documentation

The mistake: Missing key documents or failing to keep compliance records up to date.

The new framework places greater emphasis on transparency, traceability and tenant rights, meaning documentation is more important than ever.

Essential documents include:

-

Gas Safety Certificate (annual; must be valid on the day of move-in)

-

Electrical Safety Report (every 5 years)

-

Energy Performance Certificate (EPC; must be Rating E or above)

-

Deposit protection details within 30 days of receiving the funds

-

“How to Rent” guide (or updated equivalent under new rules)

-

Written tenancy agreement aligned with new legislation - verbal tenancies will be illegal

How to avoid this mistake:

-

Create a compliance checklist and calendar

-

Store documents digitally and securely

-

Ensure tenants receive all required documents at the correct time - keep a record of this

-

Review processes regularly as legislation evolves

The bottom line? Organisation and documentation are key under the new Renters’ Rights Act. Missing paperwork can invalidate possession claims or lead to penalties.

5. Assuming you don’t need professional support

The mistake: Trying to manage everything independently without fully understanding the new legal landscape.

With increased complexity and regulation, landlords face a higher risk of unintentional non-compliance.

Do you need a letting agent? Not necessarily - but professional support can be highly beneficial in keeping you compliant.

Benefits of using an agent:

-

Up-to-date knowledge of legislation

-

Handling of rent reviews, notices and compliance

-

Access to vetted contractors and maintenance services

-

Reduced administrative burden

-

A third party not emotionally linked to the property

If you’re self-managing, consider:

-

Membership of a landlord body (e.g. NRLA)

-

Training and qualifications

-

Legal support services

-

Property management software

Whether through an agent or support network, staying informed is essential.

Final thoughts

The Renters’ Rights Act doesn’t remove landlords’ rights - but it does require a more structured, professional and compliant approach to property management.

By avoiding these 5 common mistakes, you can:

-

Protect your investment

-

Maintain positive tenant relationships

-

Stay on the right side of the law

In a more regulated market, success will increasingly depend on knowledge, preparation and attention to detail.

Key takeaways

- With the abolition of Section 21, landlords must rely on structured Section 8 grounds, accurate notice periods and bulletproof documentation to regain possession.

- Informal or frequent rent hikes are no longer permitted. Rent increases are limited to once a year, must reflect local market rates and require the correct written notice.

- Strict timelines for property repairs and up-to-date documents are essential to avoid penalties and ensure possession claims aren't invalidated.

Demystifying Your Rental Contract: A Professional Overview

If you’re entering a new tenancy, be aware that from 1 May 2026 all agreements will move to Assured Periodic Tenancies, replacing fixed-term contracts. Understanding this change will help you manage your tenancy with confidence.

Let’s be candid, most people skim contracts and move on. However, a rental agreement warrants closer attention.

From 1 May 2026, all private tenancies—both new and existing—will transition to Assured Periodic Tenancies (APTs). While you may be familiar with rolling agreements, the updated structure introduces notable changes.

It is essential to review the terms carefully before signing. Below are the key points to consider.

Your new Assured Periodic Tenancy

Fixed-term Assured Shorthold Tenancy agreements (ASTs) will not exist from 1 May 2026. They will be replaced by APTs.

APT contracts apply when:

-

The rent is more than £250 per year (or more than £1,000 if you're in London)

-

The rent is less than £100,000 a year

-

The landlord does not live in the same building

-

You have exclusive occupation

If you are offered a fixed-term AST from 1 May 2026, you can make a complaint to your local authority.

What your APT must contain

APTs issued from 1 May 2026 must contain the following information:

-

The date the tenancy starts

-

How much rent is being charged and the date it is due

-

Details of other payments you are expected to make, such as utility bills

-

The landlord’s details and your details (this could be multiple names if the property is jointly owned or you’re renting with others)

-

Information about the property, including its full address

-

The amount of security deposit that is due

-

Information on how you can end the tenancy

-

Information on how your landlord can end the tenancy

-

A statement that explains your landlord is obliged to provide a property that’s safe and fit for human habitation

-

How you can request to keep a pet or make adaptations to the property

-

A statement that confirms your landlord must use a Section 13 notice to increase the rent

Your landlord could also send you this information as a written statement before you sign the contract.

Joint or sole tenancy?

Your APT will either be a joint or sole tenancy agreement.

A joint tenancy agreement means everybody in the rental home is collectively responsible for paying the rent.

A sole tenancy agreement means you have an individual contract with the landlord and you are only liable for your portion of the rent.

Which one is right for you will depend on what kind of home you’re renting and who with.

If you’re moving into a smaller house share with friends or a family rental home, you’ll probably have a joint agreement.

If you’re moving into a large property with lots of rooms rented by people you do not know, a sole tenancy might be more appropriate.

Are the personal details correct?

All details must be correct for the contract to be valid. Check that your name, the landlord’s name, contact details for both parties and the property’s address are all present and spelt correctly.

What about the dates?

Your agreement should include the date your tenancy begins but remember, APTs have no fixed end date. This allows you to leave the property when it suits you, as long as you give your landlord two months’ notice.

Do the rates and fees all stack up?

It sounds obvious but double check the monthly (or weekly) rental rate and what date it needs to be paid. You might want to set up a direct debit to make sure you never miss it.

The Renters’ Rights Act will change how much rent in advance your landlord can ask for. This will be capped to one months’ rent.

Security deposits remain unchanged. You’ll be asked for up to 5 weeks' rent if your annual rent is less than £50,000, or up to 6 weeks' rent if your annual rent is £50,000 or greater.

Do you know the notice period?

APTs will contain a brand new notice period. From 1st May 2026, you’ll need to give your landlord two months’ notice to quit, which can be served on the day you move in. Break clauses will no longer apply.

Who's paying the bills?

Normally the renter pays their own bills, such as utilities, broadband and council tax. Exceptions can include student lets or when the property is advertised as ‘bills included’.

Your contract will tell you what bills you are expected to pay, if any, and whether you’re allowed to switch utility providers.

Is it clear about repairs?

Your contract will outline who is responsible for what repairs. Your landlord will usually fix general wear and tear, as well as structural issues.

If you cause any damage, expect to pay for the repair yourself.

Don’t assume all maintenance jobs are your landlord’s responsibility. You may be liable for clearing out gutters and unblocking drains, so read the contract carefully.

You are also entitled to see a Gas Safety certificate and an Energy Performance Certificate (EPC) for the property.

Any extra rules?

Your landlord will use the APT to set out extra conditions and rules. For example, storing bikes inside, smoking on the property or even drying laundry indoors could be banned.

There might also be rules around whether you can decorate (and who pays) or sublet rooms. It's also worth noting you're responsible for anyone's behaviour when they visit.

If you’re not happy with any of the rules set out in your APT, ask if they can be reconsidered before you sign.

Do you want to make any amends to the contract?

Flag up any errors and ask for amendments before you sign.

If anything sits uncomfortably with you, ask that it’s changed and be clear if it is a deal-breaking issue. Make sure the contract is updated before you sign it.

If the landlord has agreed to make improvements to the home before you move in, this should be included in the agreement.

What if something changes while you're under contract?

Life moves on, and it's not always nicely and neatly at the end of a tenancy agreement.

So what are your obligations if something changes while you’re still under contract?

A new job or losing a job

You don't usually need to tell your landlord about a change in employment, unless it's specifically stated in the contract.

But if you’re struggling to pay the rent, it’s worth talking this through with them.

If you keep paying your rent late or if there’s arrears of less than 2 months, your landlord can start the eviction process. They must give you 4 weeks’ notice to do so.

The case would go to court and a judge would decide if the eviction request is reasonable.

If you need to leave

APTs state you must give your landlord 2 months’ notice to quit, in writing.

You can serve your landlord a notice to quit on the day your tenancy starts but the notice must expire at the end of a rent period.

You may be able to negotiate an earlier exit by mutual agreement. In this case, you may still be liable for paying your rent during the notice period.

Students in Houses in Multiple Occupation (HMOs)

If you’re a student renting a room in a HMO, you can give your landlord two months’ notice to quit.

If you signed a joint tenancy, your notice to quit will end the contract for all your housemates. The whole house will need to agree on a tenancy end date.

Finding a replacement tenant

If your APT is a joint agreement and you give notice to quit, you may want to find a replacement tenant. Tell your landlord if you have found someone as they’ll need to pass referencing and affordability checks.

If you’re part of a joint tenancy where one tenant leaves, the APT will need amending or recreating when a replacement renter is found. Ask to see the new contract and read the details in case anything has changed.

Key takeaways

- Assured Periodic Tenancy (APT) agreements will be the only contracts offered

- Your APT will give you new rights and protection

- Read the agreement carefully, especially when it comes to your responsibilities

- Ask questions and request any changes before you sign

How to Respond When Your Landlord Raises Rent

How your landlord can increase rent changes on 1 May 2026. Here’s what you can expect and how to deal with a rent increase you think is unfair.

There are plenty of good things about renting but most renters - and lots of landlords - will agree that rent increases aren’t one of them.

Aside from feeling quite unfair, a rent rise can be an unwelcome dent to your budget. Probably the last thing you need right now.

But landlords have the right to increase your rent from time to time, even if they’re reluctant to do so. How landlords can do this is changing from 1 May 2026, thanks to the Renters’ Rights Act.

So let’s go through what’s changing. We’ll explain when your landlord can increase your rent, how much they can increase it by and the steps you can take to challenge a rise that feels unfair.

Can my landlord increase my rent?

Landlords will keep the right to increase your rent. The Renters’ Rights Act will, however, limit rent increases to just once per year.

Rent review clauses, which allowed landlords to increase the rent more than once a year, will be banned. If you have one of these clauses in your tenancy agreement, it won’t apply after 1 May 2026.

What will happen to my fixed-term contract?

The majority of fixed-term contracts, also known as Assured Shorthold Tenancies, will automatically become Assured Periodic Tenancies on 1 May 2026.

Any rent review clause that was in your old tenancy agreement will not apply.

How will my landlord tell me about a rent increase?

Your landlord will have to use a Section 13 notice to increase the rent.

As a tenant, you will be notified by receiving Form 4A. This will show you when your last rent increase was and what new rent your landlord wants to charge.

How much notice should I get before a rent increase?

Notice periods will be standardised for renters. You must be given two months’ notice before any rent increase takes effect.

How much can my landlord increase my rent by?

The Renters’ Rights Act is designed to stop landlords charging what they like.

Any increase must be no higher than the open market rent. The Government classes this as ‘the price that would be achieved if the property was newly advertised to let’.

What would be classed as an unfair increase?

Government guidance says: if you’re renting a two bedroom flat for £800 but similar flats in the area are renting for £1,000, it’s fair to expect a landlord to ask for the £200 per month increase.

But a proposed jump to £1,200 for this flat usually wouldn’t meet the ‘fair and realistic’ standard, so you’d be within your rights to challenge it.

Our Rental Market Report for March 2026 tells you what the average rent is in your region or closest city.

Step by step: what to do if your landlord wants to increase your rent

1. Familiarise yourself with The Renters' Rights Act Information Sheet 2026

The Renters’ Rights Act Information Sheet 2026 is a document that tells you how landlords can increase the rent, by how much and what you can do if you’re not happy with a suggested rise.

2. Read your Form 4A

This will tell you how much your landlord wants to increase your rent by. Make a note of the proposed sum.

3. Look at what similar properties are renting for nearby

The next thing to do is make sure the proposed rent increase is in line with open market rents in your area.

Search properties to rent, using the filters to find similar size, type and condition homes to yours.

Don’t forget, you can also check our Rental Market Report for March 2026 to see the latest rents and rises in your region.

Knowing what similar properties currently cost to rent is essential if challenging a rent increase.

4. Speak to your landlord or letting agent

Whatever you’ve found out so far, it’s time to have a conversation with your landlord or letting agent.

If you don’t think the proposed increase is fair, show them the similar rental properties you’ve found.

Stay calm and professional, ask questions and make sure you really understand why your landlord is increasing the rent to the suggested rate.

The letting agent will be able to help both parties see each other’s point of view and help you come to an agreement.

5. See if there’s room to negotiate on the rent increase

You can respectfully ask the letting agent if the landlord is open to negotiation if you feel the rent increase is too high.

Explain your situation and the impact an increase will have on you. Suggest a rent that you think is fair based on current open market rents.

Your landlord may negotiate on price rather than risk losing you as a tenant.

Hopefully you can reach an agreement that’s fair for you and your landlord.

What can I do if my landlord is adamant about the increase?

If you can’t reach an agreement, you have two options: cut your losses and look for a new place or challenge the rent increase.

Neither are ideal options - particularly if you love where you live - but weigh up the increased rent against the upheaval and cost of moving house.

Get support to pay your rent

Another option is looking into the financial support you could get to pay rent.

You could get help to pay rent from:

-

A budgeting loan (if you’re already on benefits)

-

A discretionary housing payment from your local council (if you’re already on benefits)

How to challenge a rent increase

You can take your challenge to the First-tier Tribunal’s residential property division.

The Government is making it easier for tenants to challenge rent rises by keeping costs low. An application to challenge a rent increase will cost £47, with no hearing fee. There will also be funding available for those who can’t afford to make a challenge.

Be aware, the tribunal may rule in your landlord’s favour. The Renters’ Rights Act will, however, ban tribunals from increasing the rent beyond the landlord’s suggested increase.

Keep paying your rent on time - but not at the proposed higher rate

Make sure you apply to the tribunal before the increased rent is due to start. This date will be on the Form 4A.

Keep paying your usual rent while waiting for the tribunal’s decision, otherwise you could fall into rent arrears and face eviction.

But don’t pay the proposed higher rate until the tribunal gives its decision. You could be seen to have agreed to the new rate if you do.

Backdated higher rent payments will be banned, even if your challenge is unsuccessful. The new rent will only apply from the date of the tribunal’s decision.

How the tribunal works

First-tier Tribunal hearings are normally overseen by a legally-qualified judge and a panel of tribunal members. It is the tribunal who decides what a fair rent is.

They’ll look at your current rent, what your landlord wants to increase this to and the current open market rent for a similar property where you live. This will help them decide if the rent increase is fair.

Tribunals will receive a new power to defer rent increases by up to a further two months in cases of ‘undue hardship’.

If the tribunal decides the increase is fair but you don’t want to pay it, you’ll have to move out.

You may be able to challenge a First-tier Tribunal decision by appealing to the Upper Tribunal but specialist advice is recommended.

Key takeaways

- The Renters’ Rights Act will limit rent increases to once per year

- Any increase must be no higher than the open market rent

- Rent review clauses will be banned

- Your landlord must use a Section 13 notice to increase the rent

- You must be given at least two months’ notice before a rent increase takes effect

- It’ll be inexpensive for you to challenge a rent rise if you think it’s unfair

Landlord Compliance in 2026: Navigating UK Rent Increase Rules

With the Renters’ Rights Act coming into force on 1 May 2026, informal rent adjustments are no longer permissible. Landlords are now required to adhere to formalised procedures, ensure any increase aligns with prevailing market rates, and provide extended notice periods in order to remain fully compliant with the law.

With the Renters’ Rights Act coming into force from 1 May 2026, rent increases are about to get far more regulated.

The Act introduces clearer rules designed to protect tenants from unfair or excessive rises.

Rent increases are now a more formal legal process governed by strict rules.

For landlords, this means rent reviews must be approached carefully and formally. But with the correct procedures and market evidence, you can adjust rents confidently while staying within the law.

How often can I increase rent under the Renters’ Rights Act?

In most cases, rent can only be increased once per year. And there can be no increase within the first 52 weeks (1 year) of a new tenancy.

This removes the flexibility you might have previously relied on and reinforces the need to set realistic rents from the outset.

Contractual rent review clauses written into tenancy agreements will be abolished and rendered void under the new Act.

Attempting to increase rent more frequently, or without following the correct statutory process, could result in disputes or legal challenges.

Kristjan Byfield, Mission Commander at The Depository, issues a word of advice for landlords planning a rent increase:

“How your tenants are cared for during their tenancy will likely dictate how your rent review process will go. Make sure you have tenants that genuinely love living in your homes - and be fair when reviewing the rent.

“Tenants are about to decide when they leave and what a rent review process looks like, so give them every reason to stay.”

Let’s get into the rules about increasing rent under the Renters’ Rights Act.

When do I need to use a Section 13 notice?

Informal agreements, such as verbal conversations or casual emails, are no longer sufficient.

As all tenancies will convert to periodic (rolling) tenancies, you must always use the prescribed legal mechanism: a Section 13 notice.

This is a formal statutory document that clearly sets out the proposed new rent and the exact date it will take effect.

Finally, you should keep detailed records of all rent reviews, communications and any Section 13 notices you have served. This not only supports compliance but also provides protection in the event of a dispute.

How much can I increase rent under the Renters’ Rights Act?

You can increase rent up to the current fair market rate. That means you should go by what the property would fetch if it were newly advertised to let today.

Before proposing an increase, research local market rents and be prepared to justify your decision.

Letting agents can provide useful benchmarks, helping ensure your figures are realistic and defensible.

Under the new system, tenants have stronger rights to dispute rent increases they believe exceed market value.

These challenges may be referred to a First-tier Tribunal, which will assess whether the proposed rent aligns with comparable properties in the area.

Crucially, the Tribunal can no longer set the rent higher than what the landlord initially proposed, meaning tenants effectively have ‘nothing to lose’ by challenging a hike.

The Tribunal will also no longer backdate increases, and the new rent will only apply from the date of the Tribunal's decision.

When you’re thinking about increasing rent, it’s worth considering tenant relationships. While the law may allow for an increase, large or sudden jumps can lead to dissatisfaction, increased turnover and void periods.

That means a measured, market-aligned approach will be more sustainable in the long term.

How much notice must I give before increasing rent?

Under the Renters' Rights Act 2025, the mandatory notice period for a Section 13 rent increase has been extended. You must provide your tenant with 2 months' written notice before the new rental amount comes into effect.

This notice period gives tenants more time to review the increase and, if necessary, challenge it.

How can a letting agent help with increasing rent?

Navigating the new legal landscape of the Renters' Rights Act can feel daunting. Rent reviews are now a strictly regulated legal procedure, so leaning on a professional letting agent can help protect your investment.

A good agent takes the guesswork out of the process by providing accurate, evidence-based market valuations. Since the new rules cap rent hikes at the current market rate, an agent’s access to hyper-local data ensures your proposed increase is fair, defensible and less likely to be challenged at a tribunal.

If a tenant does dispute the increase, your agent will be invaluable in compiling the necessary portfolio of comparable properties to justify the new rent. This handles any pushback objectively, preserving your relationship with the tenant and turning a potential legal minefield into a smooth, fully documented process.

Kristjan’s top tip for those already using a letting agent? Take this chance to get your tenants’ perspective.

“If you have a managing agent, now might be a good time to reach out to your tenants directly to see what their rental experience is like. There’s nothing like hearing things first hand and the Act means that great rental experiences will be even more vital in shaping top-performing property portfolios.”

Key takeaways

- From 1 May 2026, rent cannot be increased within the first year of a tenancy, and only once a year after that, using a Section 13 notice.

- Proposed increases cannot exceed the current fair market rate.

- Tenants now have stronger, risk-free rights to challenge hikes at a tribunal.

- You must give tenants a full 2 months' written notice before an increase takes effect.

- Documentation, market research and professional support can help you adjust rents while staying within the law.

The Renters' Rights Act: What It Means and How to Prepare

As the Renters’ Rights Act comes into force, it brings wide-ranging implications across the lettings market. This guide breaks down the core changes, from eviction reforms to rent controls and tenant rights regarding pets.

Do you know how the Renters’ Rights Act will affect your tenancy? Thinking of renting but not sure what the new legislation means?

Our guide to what’s changing will help you navigate your renting journey, whether you're new to renting, an existing tenant or a landlord.

What is the Renters’ Rights Act?

The Renters' Rights Act 2025 is a landmark piece of UK housing legislation designed to reform the private rented sector.

Having received Royal Assent in October 2025, the Act represents the most significant update to tenant and landlord laws in nearly 40 years.

The Act comes with a lot of changes that will affect both landlords and tenants. Its primary purpose is to rebalance the rental market, providing more security and stability for private renters across England.

When does the Renters’ Rights Act start?

The Renters’ Rights Act will come into effect in phases. The first big milestone is 1 May 2026, when we’ll see changes like new rules for evicting a tenant and the switch from fixed terms to periodic tenancies.

There will be more changes later in 2026, including a new ombudsman. And beyond that, there will be new EPC rating requirements and a Decent Homes Standard.

Renters’ Rights Act changes from 1 May 2026

New eviction process

Your landlord will need a valid reason to evict you, known as a ground for possession. You can find a list of the new, revised and existing grounds on the government’s website. There are new notice periods too, which may allow you to stay in your home for longer.

Landlords will still be allowed to sell their property but they won’t be able to use this reason during the first 12 months of your tenancy. In addition to waiting 12 months, your landlord must give you at least 4 months’ notice.